When companies design a card program funded in advance, the reloadable vs. non-reloadable question is treated as a product decision based on:

- How much flexibility do users need?

- Will the card be used once or many times?

- Is this meant to feel like a gift card, a payout, or an ongoing account?

While these questions are important to the business strategy, they don’t always take into account one of the biggest implications of the decision, which is whether or not individual cardholder KYC will need to be built into the program.

The difference between reloadable and non-reloadable prepaid cards is a regulatory fork in the road. The choice shapes onboarding flow, timeline, approval process, data requirements, compliance obligations, and the overall experience your cardholders will have before they can access funds.

This is why this decision shouldn’t wait until late in the process, after cards have been ordered or the user experience has already been mapped. It should be made at the design stage, so that you can properly plan for any subsequent steps.

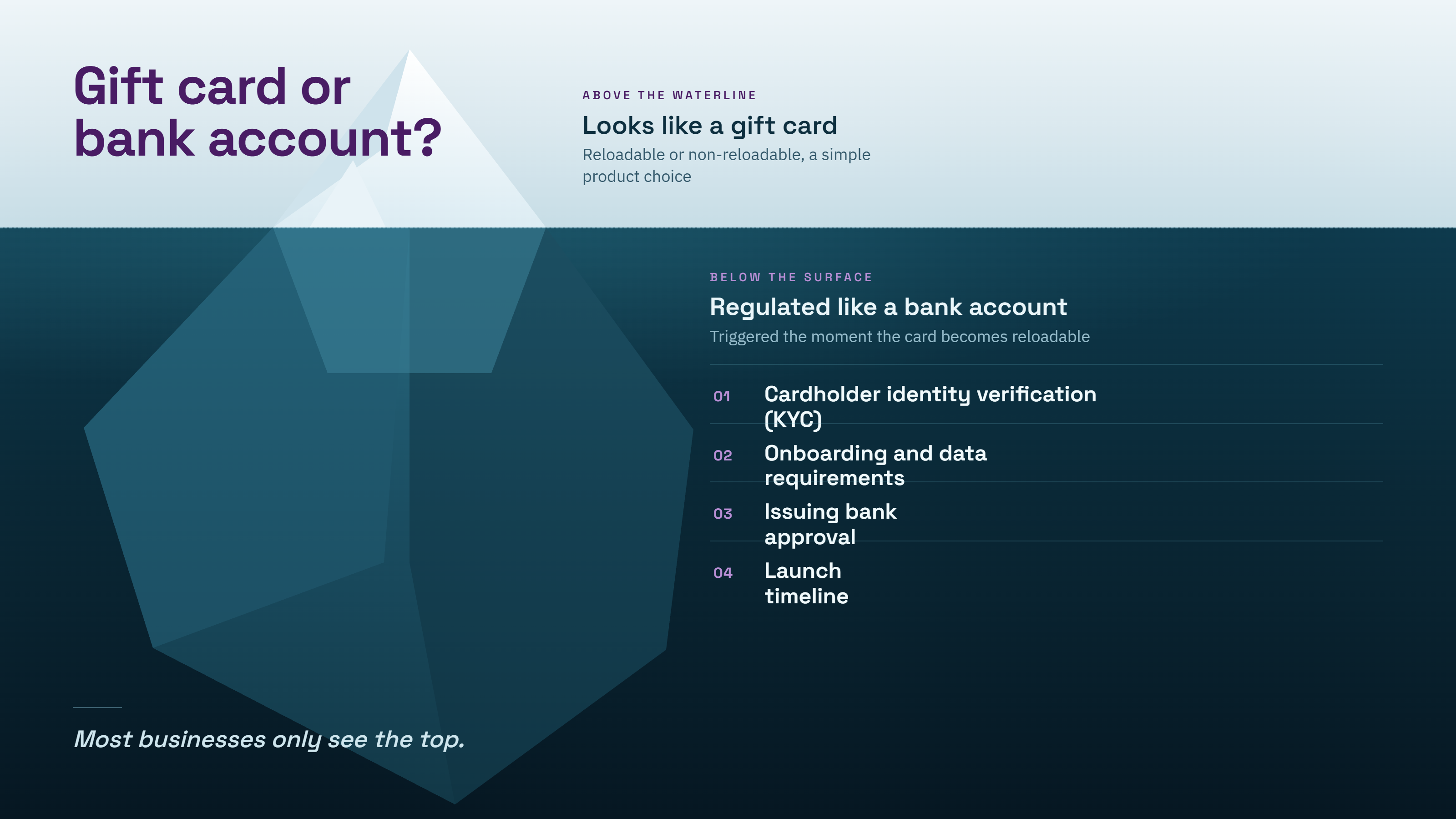

Two Card Types, One Regulatory Fork

Prepaid cards can either be non-reloadable and only used once, or reloadable which allows them to be used multiple times.

Non-Reloadable Prepaid Cards

A non-reloadable card is issued once, loaded up with a certain amount of funds, spent down, and then discarded or allowed to expire.

The best way to think of this is like a gift card or one-time payout. The value is fixed at issuance and the cardholder spends the funds and that’s it. The card is not meant to become an ongoing financial relationship.

The key point is that once the card is funded, it can’t be funded again, and therefore no KYC is required.

Reloadable Prepaid Cards

A reloadable card can receive funds multiple times over the life of the card.

Instead of being a one-and-done payment product, a reloadable card functions more like an account relationship. The cardholder may receive repeated payments, maintain a balance, access an app or a portal, track transactions, transfer funds or use the card as an ongoing financial tool.

That repeat funding capability is what changes the compliance analysis.

Why do Reloadable Cards Trigger KYC?

The reason reloadable cards trigger KYC comes down to anti-money laundering (AML) logic.

A one-time, capped-value card creates limited exposure. The amount is known, the use is finite, and the existence of the card doesn’t create a long-term financial relationship with the cardholder.

A reloadable card is different. Once funds can be added again and again, the card starts to look less like a gift card and more like an account. And ongoing accounts can create opportunities for money laundering, terrorist financing, fraud, and other misuse risks that regulators, issuing banks, and card networks need to control.

In the United States, you might hear the term CIP (customer identification program) rather than KYC (know your customer). In Canada, the relevant language could be client identification under FINTRAC requirements. In practical terms, the business impact is if the card structure creates an account-like relationship, the issuing bank or regulated financial entity may need to identify the cardholder before the card can be fully used.

This is why a reloadable prepaid card program usually needs identity-verification as part of its workflow. This process may include collecting personal information, verifying the cardholder, handling failed verification attempts, creating exception processes, and ensuring that the user experience clearly explains why the information is required.

For businesses considering a prepaid card program, the lesson is straightforward: if your business model depends on repeatedly funding the same cardholder, you should assume that KYC or client identification will need to be part of the onboarding flow.

The Non-Reloadable Exception (And Its Cap)

Non-reloadable cards can generally avoid individual cardholder KYC because the exposure is capped and nonrecurring. But that doesn’t mean that “non-reloadable” automatically means “no compliance obligations.”

The exact treatment depends on the jurisdiction, the card network, the issuing bank, the card’s value, whether it is open-loop or closed-loop, whether it can be used internationally, whether transfers are permitted, and whether the program has other account-like features.

The practical takeaway is not that every low-value non-reloadable card is automatically outside every requirement. It is that a properly structured, capped, non-reloadable program may be able to avoid individual cardholder KYC because it doesn’t create the same ongoing account relationship.

A reloadable program, by contrast, is much more likely to require identification because the relationship continues beyond that first load.

Examples of Each Model

The right structure to choose depends on the specific use case.

Reloadable Model: Better for Ongoing Relationships

Reloadable cards make sense when the same person will receive funds repeatedly or when the sponsor wants the card to become a persistent payment touchpoint.

For example, an employee recognition program may want to reward the same employees over time. Or, a sales incentive program will fund the same dealer, broker, or channel partner each time they hit a target. A gig worker payment program also pays the same worker after every shift or completed job.

In cases like the above, the reloadable model creates a better long-term experience. The recipient can keep the same card, maintain access to a branded portal or app, track activity, and receive future payments without being issued a new card each time.

The sponsor just needs to account for the added compliance layer from the outset. If the cardholder needs to be verified, that requirement must be built into the onboarding experience from the beginning.

Non-Reloadable Model: Better for One-Time Distribution

Non-reloadable cards are a better fit when the payment is single-use, capped, and tied to a specific event or campaign,

Examples include live event giveaways, kiosk-based disbursements, one-time promotional rewards, rebate programs, and certain instant issuance scenarios where walk-up recipients need immediate access to a defined amount of funds.

In these cases, the sponsor is not trying to establish an ongoing relationship with the cardholder. The goal is simply to distribute funds quickly, securely and with clear limits. A non-reloadable card can reduce onboarding friction and make the program easier to execute at scale.

The tradeoff is flexibility - if the recipient needs more funds later, you have to issue a whole new card rather than just adding funds to the same one.

4 Questions to Help You Choose A Prepaid Card Structure

Before deciding whether to create a reloadable or non-reloadable prepaid card structure, ask these four questions:

Will the same person receive funds more than once?

If yes, a reloadable card is likely to be the better fit, and you should assume that individual cardholder verification might be required.

If no, a non-reloadable card may be enough.

Could the total value per person exceed the non-reloadable cap?

If the expected value is low and capped, a non-reloadable structure may work well, but if the value may grow over time or vary significantly by recipient, a reloadable structure and the accompanying compliance additions may be more practical.

Do you need an ongoing relationship with the cardholder?

If the cardholder needs app access, ability to track spending, mobile wallet use, transaction history, future loads, or account-style features, the program is moving towards a reloadable model.

If, however, the cardholder only needs to receive and spend a one-time amount, a non-reloadable model may be simpler.

Is speed more important than flexibility?

Non-reloadable programs are usually faster and simpler to implement because they can reduce onboarding friction. Reloadable programs take more planning because of the more involved compliance and monitoring layers.

If you answer yes to reloads, higher values, ongoing engagement, or account-like functionality, you should plan for a reloadable card and build KYC into the program from the beginning.

Make the Reloadable vs. Non-Reloadable Decision Early

The most important point is timing. Choosing a reloadable vs. non-reloadable card is not a detail to finalize after the program has been designed. It is one of the decisions that shapes the program.

This decision impacts:

- Whether cardholder KYC is required

- How onboarding will work

- Which data must be collected

- How quickly recipients can access funds

- What limits may apply

- Whether the card can support future loads

- What the issuing bank needs to approve

- How much operational support the program requires

If you make the decision early, you can design the right experience from the start. If you make it too late, you may need to rework onboarding, compliance, cardholder communications, limits, and launch timelines. So make sure you are clear on whether you’re creating a one-time payment product or an ongoing account relationship.

Berkeley can help map your specific use case to the right prepaid card structure, whether that means a fast non-reloadable program, a fully reloadable cardholder experience, or a hybrid model that supports both. Let’s discuss what’s right for you.