Within a business, money is constantly in motion. Contractors get paid, claims are settled, incentives are issued, vendors are reimbursed. In large organizations, that can mean thousands of transactions happening in the background every day.

Moving money has historically been a complex process involving multiple steps from logging into bank portals and uploading files to triggering batches and checking statuses. Entire workflows have been built around the act of moving money, separate from the systems where the actual work takes place.

That separation between financial processes and core business operations has become a source of friction as companies become more software-driven. Payments aren’t a side process - they’re integral to how a business operates, and the expectation is that they should move just as quickly and seamlessly as every other business activity.

To address this friction, financial capabilities are now being built directly into the software businesses already use to run their operations. This shift is part of the rise of embedded finance, where payments, card programs, and fund distribution are integrated into workflows rather than handled separately.

Making that possible requires APIs (Application Programming Interfaces) - the building blocks that allow software platforms to connect directly to financial infrastructure and control how payments behave within their own systems. Instead of sending users to a bank or external system, businesses can build payment functionality into their own products and trigger it at the moment it’s needed.

In this article, we’ll look at how payment APIs work, what they enable, and why they’re becoming the distribution layer for financial products.

How Payment APIs Work in Practice

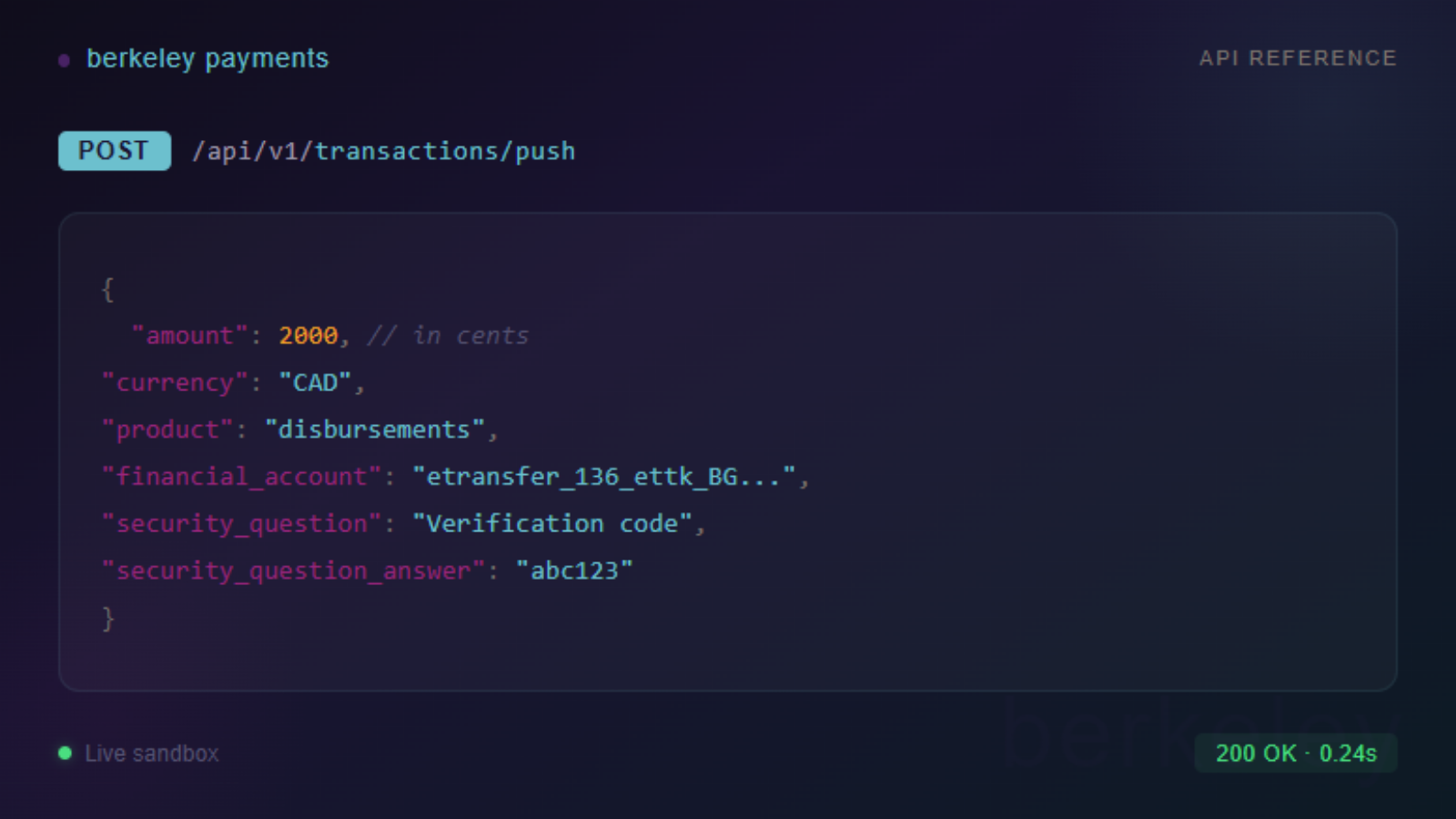

An API serves as a communication layer, enabling distinct software systems to connect, interact, and exchange instructions to work together. When it comes to payments, that means a company’s platform can connect directly to a payments provider and trigger financial actions from within its own system.

For example, if a company is running a payroll platform, it can send instructions like:

- “Pay this worker”

- “Load funds onto this account”

- “Issue a card for this user”

Once that request is sent, the payments infrastructure takes over. What looks like a single action on the surface is actually a coordinated set of processes happening in the background that includes:

- Validating the request: The system checks that the instruction is complete, authorized, and formatted correctly

- Verifying funds and balances: Ensuring there is sufficient funding available to complete the transaction

- Applying program rules: Enforcing controls such as spend limits, usage restrictions, or eligibility conditions

- Routing the transaction: Sending the payment through the appropriate network, whether that’s card rails or bank transfers

- Running compliance and fraud checks: Screening the transaction to meet regulatory and security requirements

- Returning a response: Sending confirmation back to the platform with the outcome of the transaction

All of this happens in seconds, without the user needing to leave the platform. From their perspective, the payment is simply part of the workflow they’re already in.

This allows financial capabilities to be embedded directly into software. The platform handles the experience, while the underlying infrastructure handles the complexity.

From Manual Payments to Event-Driven Workflows

One of the most important shifts enabled by payment APIs is that transactions can be triggered automatically by events inside a company’s software instead of being initiated manually.

In a traditional setup, payments sit at the end of a process. Once work is completed or a decision is made, someone still has to manually log into a system and trigger the transaction. That extra step can introduce delays, extra admin, and opportunities for error.

With API-driven infrastructure, that gap disappears, allowing payments to be tied directly to specific actions or conditions within a platform. When something happens, the system doesn’t wait for a follow-up step, it just completes the workflow automatically.

That shift may sound subtle, but it changes how businesses operate. When payments move from being a separate task to becoming a built-in function of the product itself, the impact is significant:

- Gig and contractor payments: When a job is marked as complete in a platform, funds can be loaded instantly onto a prepaid account or sent via real-time transfer. There’s no need to batch payments or run payroll cycles for short-term work.

- Insurance claims: Once a claim is approved, the system can automatically issue and fund a digital card for the policyholder. Instead of waiting days for a payout, the customer can access funds immediately.

- Sales incentives and rewards: A reward card can be generated and delivered without manual processing as soon as a milestone is achieved. This makes incentive programs faster to execute and easier to scale.

- Disaster relief and field operations: When eligibility is confirmed, organizations can instantly activate and fund cards for beneficiaries. In time-sensitive situations, removing delays can have a direct real-world impact.

In each of these examples, the pattern is the same. A business event triggers a financial action, and that action is executed automatically through the platform.

This is what makes APIs so powerful. Not only do they speed up payments, but by embedding them directly into workflows, they turn financial transactions into a seamless part of how the business operates.

Why Enterprises Prefer the API Model

As companies embed financial capabilities into their platforms, APIs are becoming the preferred way to build and manage payment programs.

Several advantages are driving this move:

- Faster time to launch: Building a payment program from scratch can take years and requires coordination with banks, networks, processors, and compliance providers. APIs remove much of that complexity, allowing companies to get up and running in months instead of investing heavily in infrastructure upfront.

- Greater flexibility and configuration: Traditional financial products come with fixed rules, which often force businesses to adapt their processes to the product. APIs reverse that dynamic and let companies define how payments behave within their own systems, from spend controls and payout timing to reporting and compliance settings, making it easier to design solutions around specific use cases.

- Ownership of the product experience: With APIs, the end user never has to leave the platform. The company maintains control over branding, customer relationships, and the overall experience, while the payments infrastructure operates in the background.

- Reduced operational overhead: By removing manual steps and embedding payment controls directly into the platform, APIs help streamline processes and reduce the need for ongoing administrative work. This lowers the risk of errors and makes payment operations easier to manage at scale.

- Scalability across use cases: Once integrated, the same API infrastructure can support growing transaction volumes, new user groups, and additional payment programs without requiring a full rebuild. What starts as a single use case can expand as the business evolves.

- Better data and visibility: API-driven payments generate structured, real-time data that can be fed directly into reporting and analytics systems. This gives businesses clearer insight into how funds are being used, making it easier to monitor performance, enforce controls, and refine payment strategies over time.

Designing Payments Into the Product Experience

Payments are becoming an integral part of how products work, shaping user experience, enabling new business models, and influencing how quickly companies can move.

APIs are what make that shift possible, allowing financial capabilities to be built directly into the systems where work already happens, rather than being accessed separately.

For businesses, the focus is less on adopting APIs in principle and more on how to apply them in practice - designing payment flows that fit their use cases, support their controls, and evolve with the product over time.

Berkeley provides API-driven payment capabilities that allow organizations to embed payments, card programs, and fund distribution directly into their own platforms, with the flexibility to configure how those flows operate and scale as they grow.

If you’re looking to build payment functionality directly into your product, streamline how funds move through your platform, or create more tailored payment experiences, get in touch to explore what that could look like in practice.