Since its introduction in recent years, “AI in the workplace” has largely meant software that helps people work faster. It drafts emails, summarizes meetings, pulls reports, and nudges teams toward better decisions. Useful, but still clearly in the assistant role.

That’s changing as we’re starting to see agentic AI show up in workflows that don’t just recommend what to do next, but actually do it.

An AI agent can research options, compare vendors, choose a plan, and complete checkout. It can handle renewals, upgrades, and routine purchases without waiting for someone to press “approve.”

Once you let software take those actions, you’ve created a new reality in which software becomes a spender.

While that’s exciting for certain stakeholders, it can also be a headache for the finance department. Finance teams don’t get to opt out of accountability just because the decision was made by an agent. If an AI subscribes to the wrong tool, over-orders inventory, or gets manipulated by a bad actor, the organization still owns the outcome.

So the practical question becomes clear: how do you give software the authority to act without giving it unrestricted access to your money?

That question is pushing organizations to rethink how payments are structured, and to build guardrails that let AI move fast without exposing the business to unnecessary risk.

Why Traditional Payment Models Break Under Agentic AI

Most payment systems were built around the assumption that a human is in the loop.

It’s a person who decides to buy something, enters credentials and then later reviews a statement. Even corporate systems assume episodic activity, manual approvals, and some form of post-transaction oversight.

Agentic AI doesn’t operate that way, though. Once an AI agent is let loose, it can initiate transactions continuously. It won’t necessarily work in reviewable batches or pause to let someone double-check a dashboard before proceeding. Once granted authority, an agent will act at machine speed.

Tools that work well for human employees don’t necessarily work as well for autonomous systems. Here’s where the tension shows up:

- Corporate credit cards create open-ended exposure: Credit cards were designed for trusted employees operating within policy. When attached to an AI agent, the credit limit becomes the only real boundary. If a configuration error or bad input occurs, transactions can repeat quickly before anyone steps in. The exposure may not be intentional, but it can escalate fast.

- Bank transfers, ACH, and wires are too rigid for autonomous behavior: These methods are built for deliberate, higher-value payments with defined payees and manual setup. They assume someone is initiating a specific transaction with clear intent. That works for planned transfers, but it doesn’t work as well when an AI agent is making frequent, smaller purchases across multiple vendors in real time.

- Manual approval workflows undermine autonomy: Adding checkpoints to every transaction removes the operational advantage that agentic systems are meant to deliver. If every decision requires human review, the speed and efficiency gains disappear.

Autonomous systems require financial controls that operate at the same pace they do. Those controls need to define scope upfront, limit exposure in real time, and prevent small errors from compounding as transactions scale at machine speed.

That represents a different design problem, one that calls for payment structures built around defined authority rather than open access.

Prepaid as Financial Architecture for Autonomous Systems

If the design problem is containment at speed, then the solution has to be structural with controls embedded directly into how authority is granted.

Prepaid changes the starting point by limiting spending power upfront rather than relying on review after the fact.

When funds are allocated in advance, exposure is finite and scope is defined before an agent ever initiates a transaction. That framework aligns naturally with systems that operate continuously and at scale, because the boundaries are set before automation begins rather than corrected afterward.

For AI agents, this means operating within a defined funding pool instead of drawing from a broad corporate account or open credit line. The organization determines in advance how much authority is granted and under what conditions, which creates clarity without slowing execution.

Three structural characteristics make prepaid particularly well-suited to an autonomous environment:

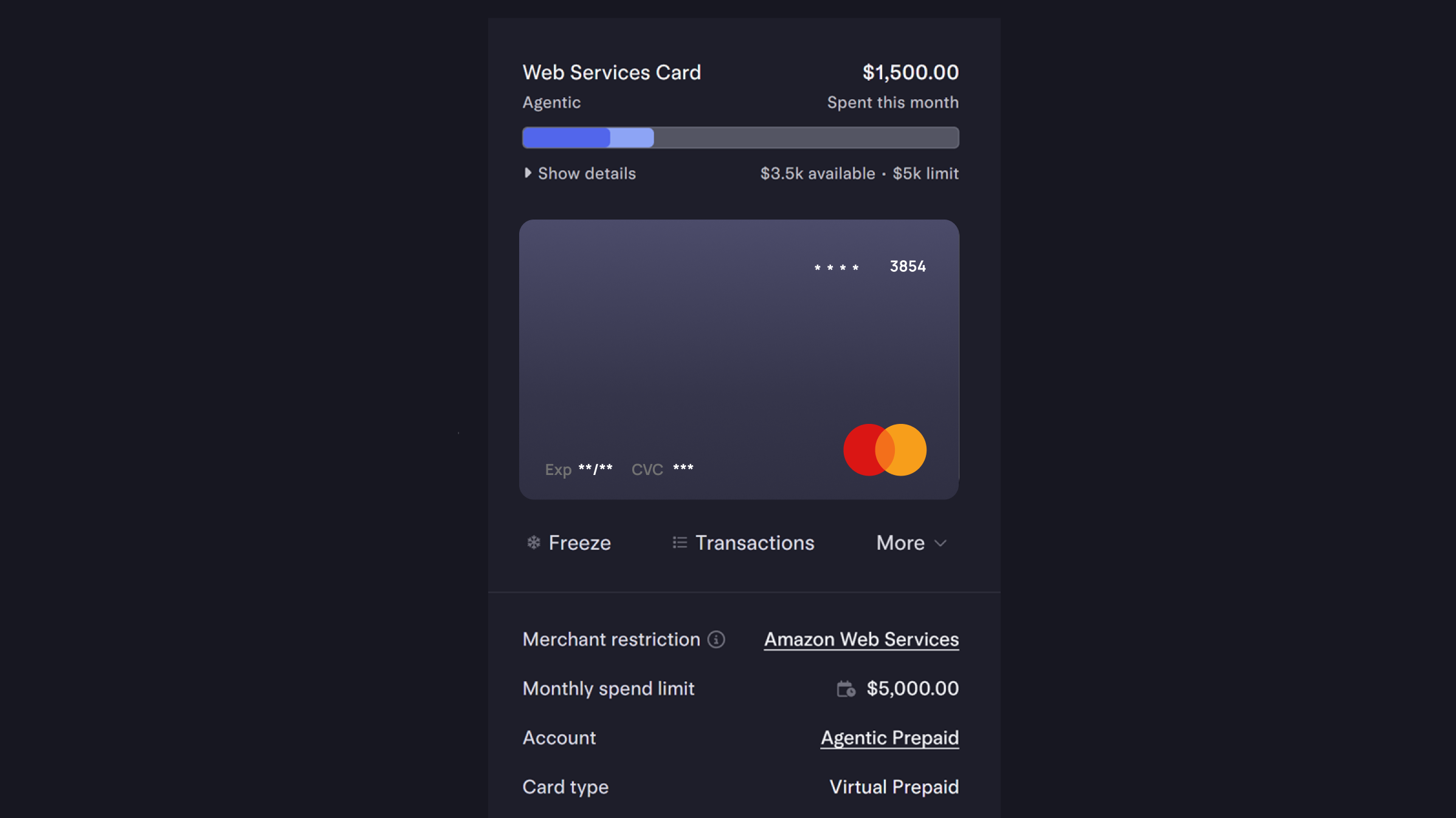

- Exposure is capped by design: An AI agent can operate only within the balance allocated to it, with no overdraft and no unintended spillover into core accounts. If something misfires, the financial impact is contained within the predefined limit.

- Rules are enforced in real time: Merchant restrictions, category controls, geographic limits, and transaction velocity caps can be configured before transactions begin. Guardrails are embedded directly into the instrument, allowing the agent to act within clearly defined parameters without requiring manual intervention.

- Authority can be scoped to role, task, or workflow: Payment instruments can be issued per agent, per function, or per job, and can be paused, revoked, or reissued as requirements evolve. That granularity supports accountability while preserving operational flexibility.

Prepaid provides a structured perimeter for automation. Instead of relying on oversight after money moves, organizations define the limits of authority before it does.

Payments Are Evolving for Autonomous Commerce

As organizations think through containment, the broader payments infrastructure is evolving in parallel. The rise of autonomous systems hasn’t gone unnoticed by networks, issuers, and platforms.

Two shifts are especially relevant:

- Tokenization is becoming the default for secure transactions: Rather than exposing full card credentials, systems increasingly rely on network-issued tokens that can be merchant-specific, revocable, and limited in scope. That reduces fraud risk and allows transactions to occur at scale without expanding credential exposure.

- Delegated payment authority is being formalized: Frameworks such as Mastercard’s Agent Pay are designed to allow AI agents to transact on behalf of individuals or businesses under clearly defined permissions. The emphasis is on traceability, identity binding, and the ability to revoke authority when needed.

While tokenization secures credentials and delegated authority clarifies who is allowed to act, prepaid addresses the remaining question of how much financial authority should an autonomous system actually have.

What Prepaid Makes Possible

When spending authority is scoped in advance, AI agents can be deployed with confidence. A defined funding pool, clear transaction rules, and revocable instruments turn autonomy from a risk into an operational tool. Instead of limiting where AI can be used, prepaid infrastructure defines where it can be trusted.

In practice, it looks like this:

- Checkout automation across dynamic merchants: As AI agents complete purchases across multiple external merchants, the control challenge shifts. Vendors may vary, transaction frequency may increase, and user-driven prompts can influence behavior. A prepaid balance assigned to the agent ensures that even in a distributed commerce environment, total spend remains within an approved range. If parameters change or activity needs review, the instrument can be paused or revoked instantly, without impacting core financial accounts.

- Subscription management that stays inside budget: AI agents already monitor software usage and adjust plans automatically. With a prepaid instrument dedicated to subscription spend, the agent can renew, upgrade, or cancel services without touching a primary corporate account. The balance allocated to that card defines the total exposure, merchant category controls restrict spending to approved SaaS providers, and finance teams get real-time visibility without reviewing every transaction manually.

- Procurement workflows aligned with supplier policy: In a B2B environment, AI systems reorder materials, source services, or purchase tools from approved vendors. Here, prepaid instruments can be scoped to specific supplier lists, departments, or budget owners. Instead of giving the system broad purchasing authority, organizations assign controlled funding pools tied to procurement rules. Spend stays within policy, aligned to a defined budget, and contained within the allocated limit.

In each of these cases, prepaid isn’t reacting to risk after it appears. It sets the perimeter before transactions occur, making it possible to give AI systems meaningful autonomy without extending unrestricted access to company funds.

Autonomy Requires Financial Boundaries

Agentic AI is moving quickly from experimentation to execution. As software begins researching, selecting, and completing transactions on its own, the structure of spending changes along with it.

Prepaid architecture offers a practical way to align autonomy with accountability. By scoping funding upfront, embedding rules directly into payment instruments, and tying authority to defined workflows, organizations can deploy AI agents without expanding access to core financial accounts.

As AI agents become part of everyday operations, the underlying payment structure becomes a strategic decision. Configurable prepaid platforms, built with granular controls and real-time visibility, provide the flexibility to support automation while maintaining financial discipline.

Berkeley Payment Solutions works with enterprises to design and deploy prepaid programs that are secure, scalable, and configurable. For organizations looking to enable AI-driven spending with clearly defined guardrails, that foundation is already in place.

Contact us to explore how prepaid infrastructure can support your AI initiatives.