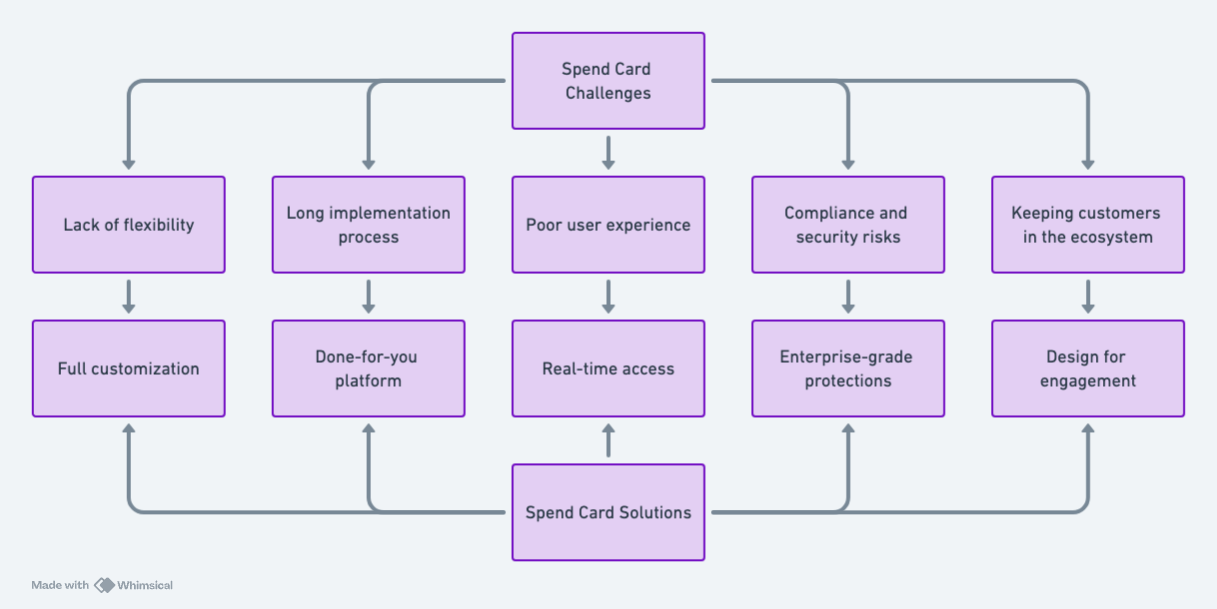

Don’t Let Spend Card Challenges Hold You Back

We’re living in an age of instant everything, and financial services are no exception. People expect fast, flexible access to their money, whether it’s for spending, saving, or investing. That puts pressure on businesses to deliver banking-like experiences - without becoming a bank themselves.

One solution that’s gaining serious traction is spend cards.

Spend cards are built to mimic everyday banking functionality by letting users access, manage, and spend funds over time, without needing a traditional checking account. Unlike one-off rewards or payroll cards, they’re designed for ongoing use. A wealth management firm, for example, might want to let clients spend from their portfolio, even if it doesn’t offer checking services. Or a business might want to provide access to a corporate expense account or a health spending wallet.

But implementing a spend card program isn’t always straightforward. It requires the right infrastructure, the right compliance framework, and the right user experience. That’s why choosing the right partner matters.

This blog explores five common challenges businesses face when trying to offer spend card programs, and how Berkeley’s platform is designed to solve them.

Challenge 1: Lack of Flexibility and Customization

For a tool that’s supposed to offer convenience, most spend card programs are surprisingly rigid. Businesses often get locked into cookie-cutter setups that don’t reflect their brand or serve their users' needs.

For businesses, that means working around the tool instead of building with it.

Common pain points include:

- Limited spending controls, such as blanket restrictions rather than fine-grained rules based on category or region

- No control over card features, like ATM access or mobile wallet compatibility

- Generic branding, where the provider’s name is front and center instead of your own

- Inconsistent user experience, with spend cards that feel disconnected from the rest of your platform or app

The result is a clunky add-on that feels like it was bolted on after the fact and not a cohesive part of the customer journey.

Berkeley’s Solution: Built for Customization

Berkeley’s platform is designed to be flexible from the outset. With over 400 configurable features, clients can tailor everything from how funds are spent to how the experience looks and feels. That includes:

- Detailed spending rules by category, geography, or merchant

- Full control over ATM access and mobile wallet enablement

- White-labeled portals and cards that reflect your brand

- Support for unique setups like a health wallet, a loan disbursement account, or a client-branded spend card for wealth management clients

Instead of making compromises, businesses can design a solution that fits exactly what their customers need and integrates seamlessly into the broader ecosystem.

Challenge 2: Long Implementation Timelines

For most businesses, setting up a spend card program isn’t just a plug-and-play situation. That’s because, unlike traditional banks, they’re not starting with the infrastructure needed to issue cards, move money, or manage compliance. And building that from scratch is no small task.

Even for companies with strong tech teams, launching a spend card offering often means navigating an unfamiliar world of banking partners, regulatory requirements, and third-party processors. Each moving part comes with its own timeline, its own vendor, and its own headaches.

The result is a rollout that can take 12 to 18 months - not because the idea is complicated, but because the execution is.

Most businesses hit delays in areas like:

- Integrating with multiple external vendors, from banks to card manufacturers

- Meeting regulatory and compliance standards, especially around fraud prevention and data security

- Testing and certifying systems, to ensure transactions flow properly

- Managing logistics, like designing, printing, and distributing physical cards

All of that adds up to a long wait during which your product roadmap stalls, customer engagement slips, and revenue opportunities pass you by.

Berkeley’s Solution: A Faster Way Forward

Berkeley simplifies the process with an end-to-end platform that’s already done the heavy lifting. Clients can go live in as little as three months, with:

- Pre-integrated partnerships with banks, processors, and card printers

- Built-in compliance support, including PCI and SOC 2 certifications

- A streamlined self-service portal for ordering and managing cards

- Expert guidance from a team that’s launched programs across multiple industries

Instead of spending a year piecing together the puzzle, businesses can move quickly and confidently, knowing the foundation is already in place.

Challenge 3: Limited Customer Control and Poor User Experience

Too often, what should be a convenient tool ends up creating friction for both users and businesses. Unintuitive or outdated interfaces make even simple tasks feel frustrating. Customers can’t easily check their balance, view recent transactions, or take basic actions like freezing a card. Real-time fund loading typically isn’t available either, so users are left waiting, sometimes when they need access to cash most.

Meanwhile, businesses have little ability to shape or enhance the experience. They’re stuck with generic portals, limited integration options, and no meaningful self-service tools. The result is a disconnected, outdated experience that reflects poorly on the brand.

Berkeley’s Solution: Real-Time Access, Branded Control

Berkeley puts both the business and the end user in the driver’s seat. The platform is designed for seamless access and intuitive control, with:

- Real-time fund loading and transfers, so users aren’t left waiting

- Withdrawal-to-account functionality, giving customers more flexibility

- Fully branded customer portals for checking balances, managing cards, and receiving real-time notifications

- Optional APIs for deep integration into your own apps and platforms

Instead of a one-size-fits-all backend, businesses can offer a polished, user-friendly experience that is an extension of their brand.

Challenge 4: Compliance, Fraud, and Security Risks

Any business offering financial products, even indirectly, is stepping into a world of complex rules, regulatory oversight, and potential fraud. And while the features of a spend card might look simple on the surface, what happens behind the scenes is anything but.

You’re dealing with personal financial data, identity verification, fund transfers, and usage monitoring - things that normally require dedicated compliance teams, certified systems, and years of operational experience. For companies that aren’t banks, it’s simply not feasible to build that kind of infrastructure in-house.

This is why trust in your platform provider matters so much. You’re relying on them to manage risk, prevent fraud, and keep your users safe. But if those safeguards aren’t built into the platform - and handled well - mistakes can be costly. Regulatory breaches, security lapses, or onboarding failures can damage both your finances and your reputation.

Berkeley’s Solution: Compliance and Security Handled for You

Berkeley brings enterprise-grade protections to every spend card program. Clients don’t need to build compliance infrastructure from scratch as Berkeley’s platform does the heavy lifting with:

- Built-in fraud prevention tools, designed to detect and block suspicious activity in real time

- PCI and SOC 2 certifications, ensuring data is stored and managed securely

- Embedded KYC workflows, including access to pre-approved identity verification providers

- Ongoing risk and compliance management, integrated into the service from day one

The result: peace of mind. Businesses can focus on the user experience, knowing the backend is secure, compliant, and built to meet industry standards.

Challenge 5: Keeping Customers and Funds in Your Ecosystem

One of the most common frustrations with spend card programs is how quickly users disengage. A card gets loaded, funds are withdrawn at an ATM, and that’s the end of the interaction. The customer is gone, along with the opportunity to build loyalty or offer additional services.

When the card feels disconnected from the rest of the experience, or isn’t easy to use in everyday life, customers naturally move their money elsewhere. They might transfer it to a personal bank account, withdraw it all at once, or stop using the card entirely after the first transaction.

That kind of behavior breaks the feedback loop. Instead of deepening the relationship, the spend card becomes a one-and-done tool - useful in the moment, but quickly forgotten.

Berkeley’s Solution: A Card Designed for Engagement

Berkeley’s platform is built to keep customers active and engaged, not just funded. By making the card useful in real-world situations and fully integrated into your branded experience, it becomes something users want to keep using. Key features include:

- Support for both corporate and customer-loaded funds, so the card can serve a variety of purposes—everything from disbursements to day-to-day spending

- Point-of-sale readiness, meaning the card works anywhere Visa or Mastercard is accepted, including physical stores, with chip, swipe, tap, or mobile wallet options

- Mobile wallet compatibility, so users can add the card to Apple Pay or Google Pay and use it straight from their phone or smartwatch

- A fully branded, user-friendly experience, reinforcing your brand every time a customer checks their balance, spends money, or receives a notification

By making the spend card more useful, flexible, and seamlessly branded, Berkeley helps businesses stay part of the financial journey and not just a temporary stop.

Berkeley Payments: From Complex to Competitive Advantage

Spend card programs don’t have to be slow, rigid, or risky. With the right partner, they can become a powerful extension of your brand, giving customers the flexibility they want and businesses the control they need.

Berkeley takes the complexity out of the equation. From rapid implementation and deep customization to built-in compliance and real-time functionality, it’s everything you need to launch a secure, scalable, and user-friendly spend card program - without building a bank from scratch.

Ready to see what’s possible? Contact Berkeley to learn how fast your program could go live.