Credit unions play a unique role in the financial system. They’re community-rooted, member-owned, and built to serve, not scale. But that same strength can also create vulnerabilities.

With smaller teams, leaner capital reserves, and a deep commitment to their members, credit unions often face greater exposure when things go wrong and have fewer buffers to absorb the impact.

According to a 2025 Federal Reserve survey, debit card fraud accounted for 39% of all fraud losses at financial institutions in 2024, more than any other payment method.

For credit unions that rely on shared infrastructure and legacy processors, the challenges are even more severe.

From direct account exposure and escalating fraud losses to high implementation costs and limited control over fraud prevention tools, traditional debit card programs are becoming harder for credit unions to justify.

That’s why more credit unions are beginning to reassess their card programs. They aren’t focusing just on how to upgrade features, but are rethinking how risk is structured in the first place. Some are questioning whether the traditional debit model still makes sense. Others are looking for ways to protect members from fraud without giving up convenience or control.

One alternative gaining traction is a Visa and Mastercard prepaid card solutions like Berkeley’s. This blog explores why traditional debit programs are falling short, how prepaid network solutions change the equation, and how Berkeley offers a modern, flexible approach that helps credit unions deliver a safer payment experience without overstretching their teams.

The Problem with Traditional Debit Cards - Especially for Credit Unions

Traditional debit card programs come with built-in risks, and for credit unions, those risks are magnified. Many of the risks and costs baked into the debit model hit credit unions harder than larger institutions because of how they’re structured, how they operate, and who they serve. For example:

- High implementation and operating costs for co-badged debit cards: Most credit unions rely on co-badged cards (partnering with a domestic network like Interac) to meet members’ expectations for online and global access. But this means absorbing multiple layers of cost such as implementation, integration, compliance, and network fees. These expenses are onerous for credit unions operating on narrower margins.

- Direct connection to members’ bank accounts increases fraud exposure: Traditional debit cards are typically linked directly to a member’s primary checking account. If card credentials are compromised through phishing, skimming, or attacks like credential stuffing, fraudsters can drain the account before anyone detects the breach. That level of exposure makes debit riskier by design.

- Fraud doesn’t just cost money: Trust is central to how credit unions operate. Member relationships are built on personal service, shared ownership, and a sense of security. When fraud occurs, it threatens more than just account balances, shaking the confidence members have in their credit union. That damage can take far longer to repair than the financial loss itself.

- Limited effectiveness of existing fraud prevention tools: Many credit unions rely on legacy providers to supply fraud detection. But these tools are often reactive, not preventative, flagging suspicious behavior after it happens rather than stopping it in real time. That lag increases the likelihood of loss.

- Smaller fraud reserves and limited capital buffers: Unlike large commercial banks, credit unions don’t have deep financial cushions. They operate with leaner balance sheets, and most are member-owned. That means losses are harder to absorb and recovery takes longer.

- Fraud losses go straight to the bottom line: Credit unions generate much of their revenue from interchange and service fees with small margins that depend on volume and consistency. Every dollar lost to fraud affects operating ratios and regulatory capital thresholds, which can limit a credit union’s ability to grow or lend.

- Shared infrastructure creates shared vulnerability: Most credit unions rely on third-party providers for card processing and fraud monitoring. When one of those systems is compromised, whether through a technical failure or a coordinated attack, the impact is felt by all the institutions at once.

The Berkeley Advantage: Prepaid Card Solution for Credit Unions

For credit unions looking to reduce fraud risk without compromising on flexibility or member experience, Berkeley’s prepaid card solution offers a strong alternative to traditional debit programs. Designed to be secure, scalable, and easy to implement, the platform helps credit unions modernize their payment offerings while protecting both their members and their bottom line.

Key Benefits of Berkeley’s Prepaid Card Solution

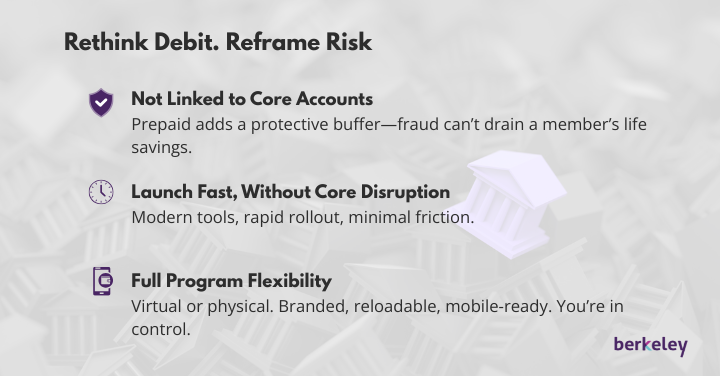

- No link to a member’s main account: Unlike traditional debit cards, prepaid cards issued through Berkeley aren’t tied to a member’s core checking account. This separation creates a vital buffer, reducing the risk of catastrophic loss if card credentials are compromised. For credit unions, it’s an easy way to offer digital-first convenience without exposing sensitive account data.

- Fraud exposure is automatically limited: Because funds are preloaded, the maximum loss is capped at the balance on the card. That structural limitation acts as a built-in safeguard, helping credit unions contain fraud without needing complex configurations or quick intervention.

- Fast, low-friction implementation: Berkeley’s platform is designed for rapid deployment. Credit unions don’t need to overhaul their systems or sink time into complex builds. With turnkey tools and dedicated support, programs can go live quickly, minimizing downtime and disruption.

- Branded, reloadable cards with flexible features: Cards can be tailored to reflect the credit union’s brand and member needs. Whether physical or virtual, reloadable or single-use, the system supports a wide range of configurations, including mobile wallet compatibility and white-labeled portals that keep the credit union front and center.

Layered Protection: How Berkeley Tackles Fraud at Every Level

Berkeley’s approach to fraud prevention is designed to work at multiple levels of the payment stack, ensuring that threats are flagged early, often before they reach the member. The different layers include:

- Custom fraud rules at the program level: Each credit union can configure its own set of rules, drawing on Berkeley’s experience to create logic that fits its member base and use cases. Suspicious activity can be flagged or blocked automatically, without relying on a one-size-fits-all model.

- Transaction-level monitoring from the processor: Every transaction goes through an additional screening layer handled by the underlying payment processor. This adds a second line of defense and helps catch patterns that might be missed by a single program.

- Oversight from the issuing bank: The bank that issues the card provides its own fraud protections and regulatory oversight, giving credit unions an added level of assurance that risk is being monitored continuously.

- Optional integration with network-level tools: For additional protection, credit unions can tap into the fraud detection systems built into Visa and Mastercard’s networks. These tools analyze massive volumes of data across the global payment ecosystem, helping to detect new and emerging fraud patterns in real time.

Why Prepaid Is the Future for Credit Unions

As fraud threats continue to grow and member expectations shift toward digital-first experiences, prepaid is a smarter long-term strategy for credit unions. Prepaid cards offer:

- Security that fits current threats: Linking cards directly to members’ bank accounts is a growing liability. Prepaid changes the equation by reducing what’s at risk from the start. That built-in limit gives credit unions a meaningful edge in protecting members and maintaining stability.

- Cost control without cutting corners: Between fraud losses, implementation fees, and the overhead of managing traditional debit systems, legacy card programs are expensive to maintain. Prepaid models shift that dynamic. They’re easier to roll out, simpler to manage, and come with fewer downstream surprises, making them a better fit for credit unions operating on tighter margins.

- Flexibility to serve members on their terms: Every credit union has a different membership base, and prepaid offers the flexibility to match. Whether it’s a fully branded virtual card experience or a reloadable physical card that supports mobile wallets, prepaid programs can be configured to meet diverse needs without reinventing the wheel.

Rethinking Risk with Berkeley Payments

Fraud isn’t an abstract risk, it’s a daily reality, and it’s putting pressure on systems that were never built for this level of threat. For credit unions, the damage goes deeper than dollars. It chips away at trust, the very foundation of the member relationship.

Berkeley’s prepaid card solution offers credit unions a way to upgrade their card programs by reducing fraud exposure, increasing control, and delivering the flexibility today’s members demand. It’s a smarter way to manage risk and strengthen your position without overextending your team.

It’s time to rethink your card strategy. Get in touch with Berkeley to explore how a smarter prepaid solution can lower your fraud exposure, strengthen member trust, and give you more control over your program.