What do groundbreaking businesses like Revolut and Apple have in common? Answer: Both companies greatly improve user experience and extend their range of services by integrating banking as a service (BaaS) into their ecosystem.

Your company can replicate these successful banking as a service examples, but only when you know how to best leverage the power of BaaS for users.

Banking as a service is dramatically changing our banking infrastructure – and along with it, banks, fintech companies, and potentially any forward-thinking business.

According to a report from financial intelligence provider S&P Global, all types of nonbank businesses that do not want to become full-fledged banks could embed financial services into their platform and customer experience through the financial technology of BaaS.

With so much potential, it’s no wonder the market of BaaS providers is growing at an impressive rate. With the BaaS market already valued at $2.41 billion in 2020, growth estimates show a promising future for the BaaS business model.

Allied Market Research, a global market research and consulting firm, projects the market size of Banking as a Service to reach $11.34 billion by 2030, an almost 5x increase from 2020.

Source: Allied Market Research

With such projected BaaS growth, and its usability within and beyond the banking industry, understanding the value BaaS can bring is crucial to future-proofing your business.

The 7 banking as a service examples in this article illustrate this to great effect. Here, we’ll cover:

- What is banking as a service?

- Who uses BaaS? 7 Banking as a Service Examples from across industries

- BaaS vs embedded finance vs open banking vs white-label

- The benefits of using BaaS

- Conclusion

Read on to learn more about BaaS.

Want to explore how banking as a service can add value to your business? Contact us to learn more about our BaaS solutions, including white-label cards, virtual cards, and tokenization.

What is banking as a service?

Before we get into examples of banking as a service, it’s important to understand the fundamentals behind the BaaS model and ask ourselves the question: what is banking as a service?

BaaS allows financial services like loans, payments, and deposit accounts to be offered as a service by tapping into the existing secure and regulated banking infrastructure. It uses modern API-driven platforms from specialist providers to deliver full banking capabilities without the need to build from scratch or even hold a banking license.

So what do BaaS providers do in layman’s terms? In essence, banking as a service providers enable third parties such as fintech companies and brands to connect directly to financial products through APIs. But what is an API?

An acronym for application programming interfaces, APIs are sets of software protocols, written in coding language, that enable different applications to communicate with each other by exchanging data requests and responses. APIs facilitate seamless connectivity between applications behind the scenes.

In terms of connectivity, BaaS solutions can easily integrate with third-party solutions via an API to either add additional services, like mobile banking and payments, or increase the functionality of existing offers.

Who uses BaaS? 7 banking as a service examples from across industries

Now that we understand what BaaS is and its place in the banking industry, let’s look at some examples of banking as a service to better see how BaaS can drive value for banks and brands, and increase user experience for end customers.

To truly grasp the scope of BaaS’ usability and value, we need to break down examples of banking as a service implemented across different industries, ranging from small companies to big brands and banks. Below are six great banking as a service examples.

1. Revolut: a global financial super app

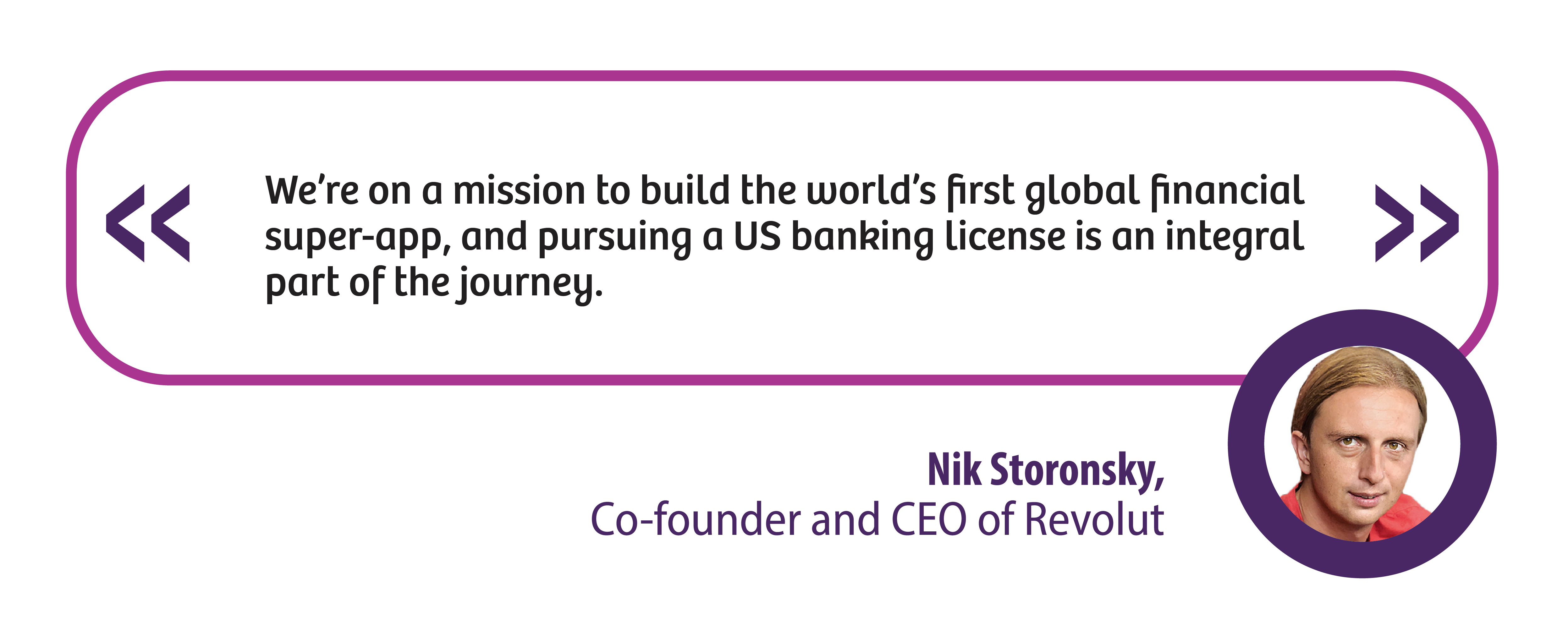

The neobank Revolut is a perfect example of how BaaS can power fintech usability and market expansion. The fintech company from the UK aims to be a financial super app that offers its services in, frankly, as many markets as it can conquer.

Just this year, the challenger bank expanded to New Zealand and Brazil, announced its personal loans product in Germany, and launched business offerings in Australia.

At the same time, Revolut has run into regulatory problems as it tries to extend its products to cover financial services that require banking licenses.

Tech.eu, an online publication dedicated to the European tech industry, writes that Revolut has yet to file a banking license application in the US while already locally serving over half a million retail customers. The bank might also get turned down for a license in the UK. Revolut owns several banking licenses in Europe.

The company’s aggressive market expansion strategy and wide range of financial services are made possible because of the neobank’s underlying financial technology. Revolut relies on an API-first architecture that allows it to integrate diverse financial services in a short time.

But while this agile architecture enables a neobank like Revolut to go through rapid iterations of its app and quickly expand to new markets, it does come with a caveat that the company is currently facing in key markets. This caveat is that there are limits to what financial services a challenger bank can offer its customers without acquiring a banking license.

2. EQ Bank: extending its financial products

As a leading savings bank, EQ Bank knew that just offering their clients high interest rates wasn’t enough of a future-proof strategy.

By integrating Berkeley’s BaaS with their existing savings account to create a one-stop wealth management debit card, their clients gained access to Mastercard payment processing, ATM withdrawal, real-time transfers, and more – all while retaining EQ Bank’s high interest rates.

By adopting the BaaS approach, EQ Bank was able to get to market quickly and grow their user base significantly.

3. Apple Card: a renowned brand integrating BaaS

Apple is in a unique position to shake up the banking business as trust in traditional banks decreases, writes Forbes. Earlier in 2023, the tech company announced that it would be offering a whopping 4.15% annual yield to savers.

As one of the world’s leading tech companies, Apple is in a unique position to offer such a yield on its Apple Card, a credit card powered by Goldman Sachs. The offer is likely to bring many of the two billion Apple users to adopt its payment services.

But more than the promise of an impressive yield, ease of use is a distinguishing factor that the marriage between major companies in tech and finance through API integration brings.

Compare applying for the tech giant’s credit card to requesting a similar product and going through KYC at a physical branch of a legacy bank. Instead, Apple users can apply for and obtain an Apple Card in a few clicks. Most customer data needed to subscribe to the credit card is pulled from the Apple ecosystem and credit scores from Goldman Sachs’ banking system.

Apple might have struck gold with this digital-first experience, where users have an intuitive banking tool at their disposal within their go-to digital environment.

The deep integration of payments and financial services, like installment loans and savings, into its native ecosystem not only improves user experience – but customer lifetime value.

4. Karat: banking the unbankable

Recently closing a $70 million investment round and partnering with Visa, Karat offers financial products in the creator space. Covered by Techcrunch, an online newspaper focusing on tech and startups, Karat aims to create a financial infrastructure for a new class of entrepreneurs who can’t rely on traditional banking.

Nowadays, creators on social media operate as businesses with teams and make serious money. Yet, many of these businesses don’t do their taxes, aren’t incorporated, and have no concept of payroll. These social entrepreneurs are thus often rejected for business accounts or credit at traditional banks.

Luckily, Karat looks at creators’ socials and financials instead of their FICO.

Through their ‘creator card’, a credit card powered by Visa, Karat creates a better-adapted financial infrastructure for this new class of businesses and helps them become financially more literate.

5. Fiverr: Powering the gig economy

According to leading consultancy McKincsey, over one in three Americans participated in the gig economy in 2022 compared to 26% in 2016. Riding that surge of independent work are job marketplaces like Fiverr.

Fiverr’s business proposal is simple: As a marketplace for digital services, the company connects small businesses and entrepreneurs with freelancers through a platform that streamlines both the workflow between parties and payment transactions.

For these services, Fiverr charges a fee on transactions – a straightforward profit model for a platform business. However, that profit model can be boosted by adding more payment transactions to the ecosystem.

Previously, freelancers on the platform would add their bank account and PayPal details to their profile to receive payments for services delivered, but the advent of BaaS allows for more direct banking integrations into the Fiverr platform through the Fiverr Revenue Card.

Powered by MasterCard through a specialist BaaS provider, this debit card enables freelancers to pay with earned funds and withdraw at ATMs around the world. In turn for providing financial ease of access, Fiverr captures additional value by earning fees over transactions that would otherwise happen in the traditional financial infrastructure and solely profited over by legacy banks.

6. Top BaaS banks in the US and Canada

While it’s important to have a deep understanding of BaaS to know how it can meet your business demands, knowing how to choose banking as a service provider is equally important. Finally, picking the right provider also means knowing which BaaS banks to choose from in North America.

When discussing BaaS banks, we can distinguish between two types of BaaS providers – BaaS banks and specialist BaaS companies (which we’ll cover in our next item on this list.)

First, traditional banks can deploy a BaaS strategy to innovate their banking services. However, many banks with retail services worry that offering their financial products through partners will threaten existing client relationships. In other words, they see BaaS as competition rather than collaboration.

In a survey among financial institutions held by Cornerstone Advisors, only 11% of banks currently deploy a BaaS strategy while a staggering 46% might consider pursuing such a strategy in the future. In business terms, ‘might consider’ is pretty far down the pipeline.

Source: Cornerstone Advisors

To further complicate the adoption of BaaS by traditional banks, these financial institutes often struggle with legacy tech and manual processes inflating costs.

For the legacy banks, the road to offering BaaS solutions requires digitalization, like deep integration of automation and APIs, and the understanding that customers look for simple and direct banking experiences, driving demand for fintech and embedded finance.

Tackling these challenges, some banks have successfully built a BaaS model into their financial infrastructure. So, what are some top BaaS banks in the US and Canada?

Goldman Sachs

One of the largest financial institutions in the world, Goldman Sachs offers its own take on BaaS with their TxB as a service, or transaction banking as a service. As stated on the bank’s company blog, third parties can access the bank’s APIs for services like payment processing, treasury automation, and data services like KYC and processing customer data.

Starling Bank

Another pioneer among BaaS providers, the UK-based Starling Bank built its BaaS service looking to primarily serve customers in the US, according to PYMTS, a global platform for analyses and news on payments and commerce. Starling Bank opened its APIs to enable banks, fintech companies, and brands to use its banking license to develop financial products like debit cards and savings accounts. The bank specializes in payment processing, or what is called PaaS (payments as a service).

Fidor Bank

While not a legacy bank, the German Fidor Bank is a neobank that operates digital-only and helps companies create digital banking solutions for their end customers. The bank also offers turnkey white-label banking products with a banking license in the US and Europe.

7. Specialist BaaS companies

Second, specialist BaaS companies offer a unique advantage compared to banks with BaaS platforms. These BaaS providers allow for a customized approach, offering different financial services from different providers.

While not banks themselves, these BaaS providers provide the financial technology and banking licenses needed for nonbanks to embed banking products into a business, brand, and tech platform.

Some of the top specialist BaaS providers include companies like Berkeley Payment Solutions.

The BaaS model compared to other banking solutions

In a 2021 consumer survey held by PWC, as much as 61% of respondents indicated they interact with banks via digital channels weekly. Meanwhile, 20-25% are forced to visit a bank branch while preferring digital channels.

This demand for digital banking solutions does not only show in consumer behavior but also in the financial ecosystem. Financial services are evolving faster than ever in this digital era.

When FIS, a global fintech company, surveyed 2,000 financial executives, 83% of respondents believed embedded finance to moderately or majorly impact business operations within a year. A potentially major disrupter, embedded finance is closely related to banking as a service. But what is the difference between BaaS and embedded finance?

It’s easy to get confused with all the new terms popping up in the world of finance. On the surface, embedded finance and open banking might seem similar to the BaaS model and do, indeed, share similarities with the latter.

For instance, digital integration through APIs and online banking are key components for all three. Let’s look at what distinguishes the various digital banking models:

Source: Business Insider

The BaaS model

Banks or specialist BaaS providers create a BaaS platform with APIs for third parties to access financial products. This model generates revenue for the BaaS platforms from the use of APIs by third parties.

These parties usually either pay a monthly fee for access to the platform or subscribe to a model in which they pay per usage of the APIs.

For banks that open up their APIs, BaaS is an inexpensive way to reach more end consumers and reduce the cost of digitalization.

BaaS vs embedded finance

Simon Torrance, a leading expert on digital business models and executive working group member of the World Economic Forum, called embedded finance a $7 trillion market opportunity in a keynote speech he delivered for FTT Embedded Finance North America. But what is it and how is it related to BaaS?

Embedded finance is essentially when nonbanks offer banking services to improve user experience and lifetime value for their customers.

BaaS is, on the other hand, the underlying financial technology that enables nonbanks to integrate banking products into their platform. Growth in the embedded finance market thus implies increased usage of BaaS platforms.

BaaS vs open banking

Are BaaS and open banking the same? Not really. Open banking also involves connecting banks to non-banks via APIs.

But, while in BaaS models, banks and nonbank businesses integrate complete banking services into their ecosystem, open-banking models and nonbank businesses merely use the bank’s data for their products.

BaaS vs white-label banking

White-labeling allows a company to use an existing product or service created by another company but sell it as its own branded offering.

Just like in other industries, white-label banking leverages BaaS platforms and rebrands the banking products to fit the fintech or brand that offers them to the end consumer.

What are the benefits of banking as a service?

For any company, be it a bank or non-bank business, building a new financial infrastructure into their platform is costly, time-consuming, and difficult. This goes especially for small businesses and startups, who usually lack the resources to invest in a full-blown financial ecosystem.

In short, more companies are using BaaS to build or enhance a business’ financial services because it’s cheaper, faster, and better.

Implementing BaaS solutions rather than building from scratch increases speed to market, lowers costs, and uses existing, reliable financial infrastructure.

Pro tip: why using BaaS is especially interesting in the US

Ever heard of The Durbin Amendment? This amendment is part of the Dodd-Frank Wall Street Reform and Consumer Protection Act that limits transaction fees imposed upon merchants by debit card issuers.

Under the amendment, small banks are allowed to charge higher interchange fees than other banks.

Bankingdive, an online publication based in Washington, DC, reports that specialist BaaS providers partner with these small banks and are thus able to both generate more interchange fee revenue for the nonbanks that use their services than a major bank would, and increase reach for small banks.

Conclusion: Tap into the power of BaaS

Banks, neobanks, fintech startups, and other nonbank financial institutions can all implement the APIs offered by banking-as-a-service providers to improve and extend their banking services.

Non-bank businesses, too, can better serve their end customers by creating a one-stop shop that offers banking products, up to a few years only offered by traditional banks, to end customers in their market niche.

As illustrated by the above banking as a service examples, the potential of BaaS services to drive revenue and increase user experience is enormous. Not just in banking, but across many industries.

Start exploring the potential that banking as a service has to offer for your company. Contact us to learn more about our BaaS solutions, including white-label payment cards, virtual cards, and more.